US tariffs implemented since 2025 have triggered profound disruptions across global commodity markets, creating price volatility, supply chain reconfigurations, and significant economic ripple effects worldwide. The impact operates through two primary channels: immediate macroeconomic effects that dampen global demand and longer-term trade reallocation patterns that redistribute commodity flows.

Agricultural Commodities: The Soybean Transformation

Soybeans Lead the Disruption

The most dramatic transformation has occurred in soybean markets, where US-China trade tensions have fundamentally reshaped global flows. China’s 44% tariff on US soybeans beginning April 10, 2025, has virtually eliminated American access to the world’s largest soybean market. US soybean exports to China, previously valued at $12.84 billion in 2024, face an unprecedented collapse.

This disruption has triggered a massive supply chain realignment. Brazil now captures 69% of China’s soybean imports, compared to less than 1% from the United States. The shift represents a 48% increase in Brazilian market share since 2017, with China’s reliance on Brazilian suppliers reaching record levels. Argentina has also capitalized on this opportunity, with soybean exports to China potentially tripling from historical levels.

![]()

Price Impacts and Market Dynamics

The trade reallocation has created stark price differentials. Without a US-China trade agreement, soybean futures per bushel**, while a resolution could drive prices to $13 per bushel. Current projections suggest average soybean prices will drop to $410 per ton in 2025, down 15% year-over-year. Meanwhile, corn prices in the US have surged 18% in 2025, reflecting ongoing tariff impacts and shifting global demand.

Broader Agricultural Commodities

Wheat faces similar pressures, with 49% tariffs on Chinese imports affecting $482 million in annual trade. Corn exports to China encounter 44% tariffs, though Mexico remains a reliable market for US producers. The agricultural sector collectively faces over $15.7 billion in US exports now subject to 44-49% tariffs from China alone.

Industrial Metals: Diverging Price Paths

Steel and Aluminum Market Splits

The metals sector exhibits the most pronounced price divergence between US and global markets. Steel tariffs of 25-50% have driven US hot-rolled coil prices up 31% year-to-date to $984 per ton, while Chinese prices declined 4% to $392 per ton. This created a $592 per ton price gap between US and Chinese markets.

Aluminum markets show even more extreme distortions. US Midwest aluminum premiums have surged 61% to a record high of $907 per ton following the implementation of 25% tariffs. The premium reflects the severe supply constraints as tariffs make imports prohibitively expensive while domestic production cannot meet demand.

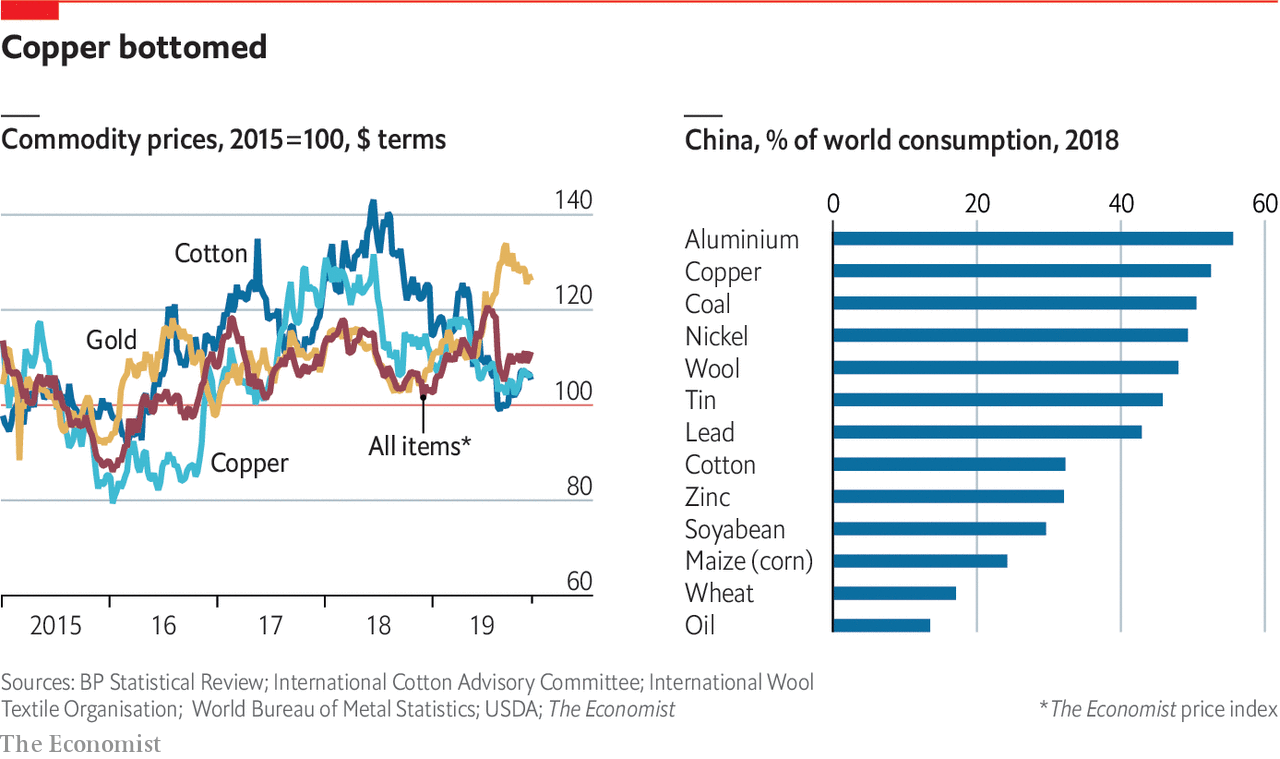

Copper Under Investigation

Copper markets face uncertainty as the US Department of Commerce investigates potential Section 232 tariffs on all copper imports. The mere announcement has driven copper prices above $10,000 per ton on the New York Comex, creating a $1,200+ per ton premium over London Metal Exchange prices. This premium could rise further if tariffs are implemented, given that 40% of US refined copper demand relies on imports.

Critical Materials: Rare Earth Restrictions

China’s retaliation includes export restrictions on seven rare earth elements beginning April 4, 2025. These elements—including dysprosium, terbium, and yttrium—are critical for defense, electronics, and renewable energy applications. With China controlling 90% of global refined rare earth supply, these restrictions threaten to create severe shortages for US manufacturers.

The restrictions represent a strategic escalation beyond traditional tariffs, potentially forcing US companies to halt production. Ford was forced to shut down facilities due to rare earth shortages, highlighting the vulnerability of US supply chains. A tentative framework agreement suggests China will provide rare earths “up front” in exchange for 55% tariffs on Chinese goods, but implementation details remain unclear.

![]()

Energy Markets: Indirect But Significant Effects

Oil Price Volatility

While oil and gas imports received exemptions from direct tariffs, energy markets have experienced severe volatility due to recession fears. Brent crude plummeted from $75 per barrel to $61 per barrel within seven days of the April 2 tariff announcement, representing a 15% decline that ranks among the three most significant three-day drops in recent history.

The decline reflects broader macroeconomic concerns rather than direct trade restrictions. JP Morgan has raised the probability of a global recession to 60% from 40% following tariff implementations. Oil markets are particularly sensitive to recession fears, as economic slowdowns directly impact energy demand.

Trade Reallocation and Supply Chain Disruption

The Brazil-Argentina Advantage

South American producers have emerged as major beneficiaries of US-China trade tensions. Brazil and Argentina are positioned to gain significant market share as China redirects purchases away from US suppliers. Brazilian agricultural exports have expanded rapidly, with the country’s infrastructure improvements, including expanded port capacity in Santos, facilitating increased shipments.

Argentina’s soybean industry faces unique dynamics, with potential imports of up to 2 million tons from Brazil in 2025 due to domestic crop shortfalls. This intra-regional trade demonstrates how tariffs create complex, multilateral adjustments rather than simple bilateral shifts.

Supply Chain Complexity

The disruptions extend beyond simple origin changes. Companies report 10-15% logistics cost increases due to tariff-induced supply chain reconfigurations. Walmart has reduced Chinese imports by 10% while increasing sourcing from Vietnam and Thailand, resulting in a 5% rise in logistics costs due to longer shipping routes.

The complexity creates significant forecasting challenges. Grain elevators and merchandisers have seen forward bookings disappear, with sales horizons contracting from 5-10 months to spot markets. The uncertainty makes it “very difficult to price a product” when tariff applications remain unclear.

Macroeconomic Transmission Channels

The Demand Channel

Tariffs operate through both direct trade effects and broader macroeconomic channels. The macroeconomic channel manifests as reduced global trade activity and economic growth, dampening aggregate demand for commodities. This effect was immediately visible in financial markets, with global stock exchanges recording average losses of 10% in the first three days after tariff announcements.

The Trade Reallocation Channel

The trade reallocation channel creates longer-lasting structural changes as excluded volumes from US markets flood other international markets. This surplus creates downward pressure on world prices for affected commodities, with impacts varying based on the commodity’s inclusion in tariff exemption lists.

Regional Economic Impacts

Latin America’s Resilience

Latin America shows resilience to US tariffs, with economic growth across most of the region remaining undisturbed. Countries like Brazil benefit from trade diversification opportunities, though the 50% tariff threat on Brazil creates new uncertainties for agricultural exports including coffee, beef, and orange juice.

Global GDP Effects

Economic modeling suggests that proposed reciprocal tariffs could reduce global GDP by 0.3-0.4%, with US GDP falling by 1-1.2%. For agricultural trade specifically, the tariffs could lead to a 3.3-4.7% contraction in global agricultural trade.

Market Adaptation and Future Outlook

Infrastructure and Investment Responses

Countries are investing heavily in infrastructure to capitalize on trade reallocation opportunities. Brazil continues expanding its Northern Arc ports to handle increased soybean exports, while transportation improvements reduce logistics costs for exporters.

Price Convergence Challenges

The sustainability of current price differentials depends on trade policy stability. Copper exemptions from certain tariff lists have already caused rapid price convergence between US and European markets, demonstrating how quickly commodity prices can adjust to policy changes.

The ongoing uncertainty suggests that commodity price volatility will persist as markets attempt to price in changing trade relationships, infrastructure adaptations, and macroeconomic adjustments. The full impact of current tariff policies will likely continue evolving as both immediate supply disruptions and longer-term structural changes work through global commodity markets.

The evidence demonstrates that US tariffs have created a fundamental restructuring of global commodity flows, with agricultural products experiencing the most dramatic shifts, metals markets showing extreme price divergence, and energy markets reflecting broader economic uncertainty. These changes represent not temporary adjustments but potentially permanent alterations to global trade patterns that will continue influencing commodity prices for years to come.